Get your credit report

It's important to know the status of your credit report, which is why we offer a free credit report. This will show you how many loans and lines of credit are currently out in your name. It also displays when these were applied for as well as any collections that may be on the account. You can also see if there are any judgments or liens against you that may affect your ability to take out new loans or lines of credit.

Check your credit report for errors

It's important to check your credit report for errors before applying for a loan, mortgage, or credit card. Errors on your credit history can make it difficult to get approved. You can request a free copy of your report from Equifax, Experian and TransUnion annually by visiting AnnualCreditReport.com. The three major companies will send you one copy every four months if you ask them to do so in writing and enclose the proper fee with their order form.

Dispute errors in your report

One of the most important things you can do to protect your credit is by checking your report and making sure it's accurate. If you find an error on your report, dispute it with the company in question. It might take time for them to investigate and get back to you, but if they remove or correct the error from their records, that will help improve your score. You can also use this opportunity to review other entries on your report and make any necessary updates or corrections.

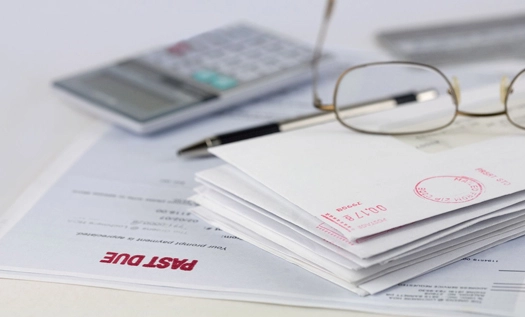

Pay late or past-due accounts

Most people are aware of the importance of a good credit score. The more positive your rating, the better your chances for approval on loans and other financing options. In order to maintain a high credit score, it's important to pay all outstanding balances in full when they come due. Otherwise, you risk damaging your credit report and hurting your financial future.

Increase your credit limits

Credit cards can be a great way to increase this number if used properly by making timely payments, keeping balances low, and paying off loans when possible. There are two ways in which they can do so: by opening new accounts with high limits (which will help show lenders that your credit is healthy) or by requesting an increase in existing accounts' limits (this would also allow more spending power).

Pay off high-interest, new credit accounts first

A credit report is a detailed summary of the financial activity in your life. This includes information about where you live, work, and how much money you make. It also includes any public records like bankruptcy filings or judgments against you for unpaid debts. The information on your credit report could affect many aspects of your life such as whether or not you qualify for a mortgage loan, car loan, or even an apartment rental lease agreement etc.

Open a new credit card

There are many benefits to opening a new credit card. For one, you can build your credit rating by responsibly using the card and paying off your balance each month. And since there is usually a sign-up bonus for opening a new account, it's worth getting another line of credit while interest rates are low. The key is not to carry over balances from month-to-month or rack up high-interest charges that will cost you more in the long run. If you think about it this way, it becomes an investment - not just buying stuff on impulse!

Pay balances on time

Many people in the US are not aware that a credit report is an important document that banks use to determine if they should be approved for loans. It contains all of your financial information including credit card balances, bank account balances, and other debt. If you have missed a payment or two then it can impact your ability to get new loans and may even lead you being denied for major purchases like a home or car so be sure to pay your balance on time!

Take Control of Your Credit Score with Credit Repair in My Area

When your credit score is holding you back from approvals, lower interest rates, or the home you want, doing nothing only makes the problem worse. With Credit Repair In My Area , you get a dedicated team that reviews your credit reports, challenges inaccurate negative items, and guides you step by step on rebuilding stronger credit habits so your score can start moving in the right direction. The sooner you act, the sooner you can work toward better offers on loans, credit cards, and other financial opportunities instead of being stuck with rejections and high costs. Take the first simple step toward a healthier credit profile and greater financial confidence by calling our credit specialists now at (888) 804‑0104 to discuss your situation and get started.

Frequently Asked Questions on Fixing Your Credit Score

1. How can I fix my credit score fast?

You can start fixing your credit score fast by paying all bills on time, reducing credit card balances, and avoiding new loan or card applications while you work on existing debt.

2. What is the first step to fixing a bad credit score?

The first step is to get your credit reports, review them carefully for errors or outdated negative items, and make a list of issues to address through disputes and repayment.

3. Can I fix my credit score myself?

Yes, you can fix your credit score yourself by disputing inaccuracies, paying on time, keeping balances low, and building a positive payment history over time.

4. How long does it take to fix a low credit score?

Many people see improvement within three to six months of consistent on-time payments and lower utilization, but deeper credit issues can take longer to fully recover.

5. Will paying off overdue debts help fix my credit score?

Paying off overdue debts can help fix your credit score because closing past-due accounts reduces risk and allows new positive payment history to carry more weight.

6. Do credit repair companies really help fix your credit?

Reputable credit repair companies can help by identifying report errors, sending disputes, and guiding your strategy, but they cannot remove accurate negative information.

7. Can Credit Repair in My Area help fix my credit score?

Credit Repair in My Area can help fix your credit score by reviewing your reports, disputing inaccurate negative items, and creating a clear plan to rebuild stronger credit step by step.